The 10% Era: Why Accelerators Are Minting Unicorns at Double the Historical Rate

Y Combinator's W26 batch is projected to produce ~20 unicorns from ~200 companies, and the Founder Institute's current cohort expects 3 to 5. The data, the playbook, and the 18-month plan Dipity is working toward with Sera.

.jpg)

The 10% Era: Why Accelerators Are Minting Unicorns at Double the Historical Rate

The 10% Era: Why Accelerators Are Minting Unicorns at Double the Historical Rate

By Morgan Von Druitt, Founder, Dipity

TL;DR: Top accelerators are now expected to turn roughly 10% of a cohort into billion-dollar companies, about double the 4.5% historical benchmark. VCs project ~20 unicorns from Y Combinator's ~200-company W26 batch, and the Founder Institute's current cohort carries a 3-to-5-unicorn expectation. Record capital ($510B in H1 2026), AI-compressed execution, and a codified visibility playbook are the drivers. Dipity is in that Founder Institute cohort, and this article ends with the 18-month plan we're working toward.

Top startup accelerators are now expected to turn roughly 10% of a cohort into billion-dollar companies, about double the historical benchmark. VCs reviewing Y Combinator's W26 batch project around 20 unicorns from roughly 200 companies, against a 4.5% historical unicorn rate that already led every accelerator on earth. The Founder Institute's current cohort, which accepted 50 founders from 1,500 applications, carries a similar internal expectation of 3 to 5 unicorns. The drivers are record capital ($510B invested globally in H1 2026), AI-compressed execution, and a codified playbook that turns founder visibility into pipeline, talent, and valuation.

Why Are Accelerators Suddenly Minting Unicorns at Double the Historical Rate?

The short answer: the playbook got codified, the execution timeline collapsed, and capital concentrated behind a smaller number of highly visible founders. For most of venture history, a unicorn was a statistical accident that took the better part of a decade. TechCrunch's midyear tally shows almost 90 new unicorns minted in the first half of 2026 alone, the fastest pace since 2021, and overwhelmingly driven by AI companies hitting the mark on compressed timelines. At the same time, Crunchbase reports global startup investment hit a record $510B in H1 2026, already more than all of 2025 combined, with AI capturing over 70% of Q2 dollars.

Three forces stack underneath that acceleration:

• Codified playbooks. Accelerators have run thousands of companies through the same system. YC alone has funded more than 5,000 companies, and the patterns that separate the winners are documented, taught, and enforced inside each batch.

• AI-compressed execution. Work that took a 40-person team a year now ships with a team of five in a quarter. The bottleneck moved from building to distribution.

• Capital concentration. Record funding is chasing a narrower set of founders, which means the companies that do get picked are resourced to grow at rates that were physically impossible five years ago.

None of this makes a unicorn easy. It makes the outcome legible, which is a different thing, and it explains why sophisticated observers are comfortable projecting 10% hit rates that would have sounded delusional in 2019.

What Does Y Combinator's Unicorn Data Actually Show Year Over Year?

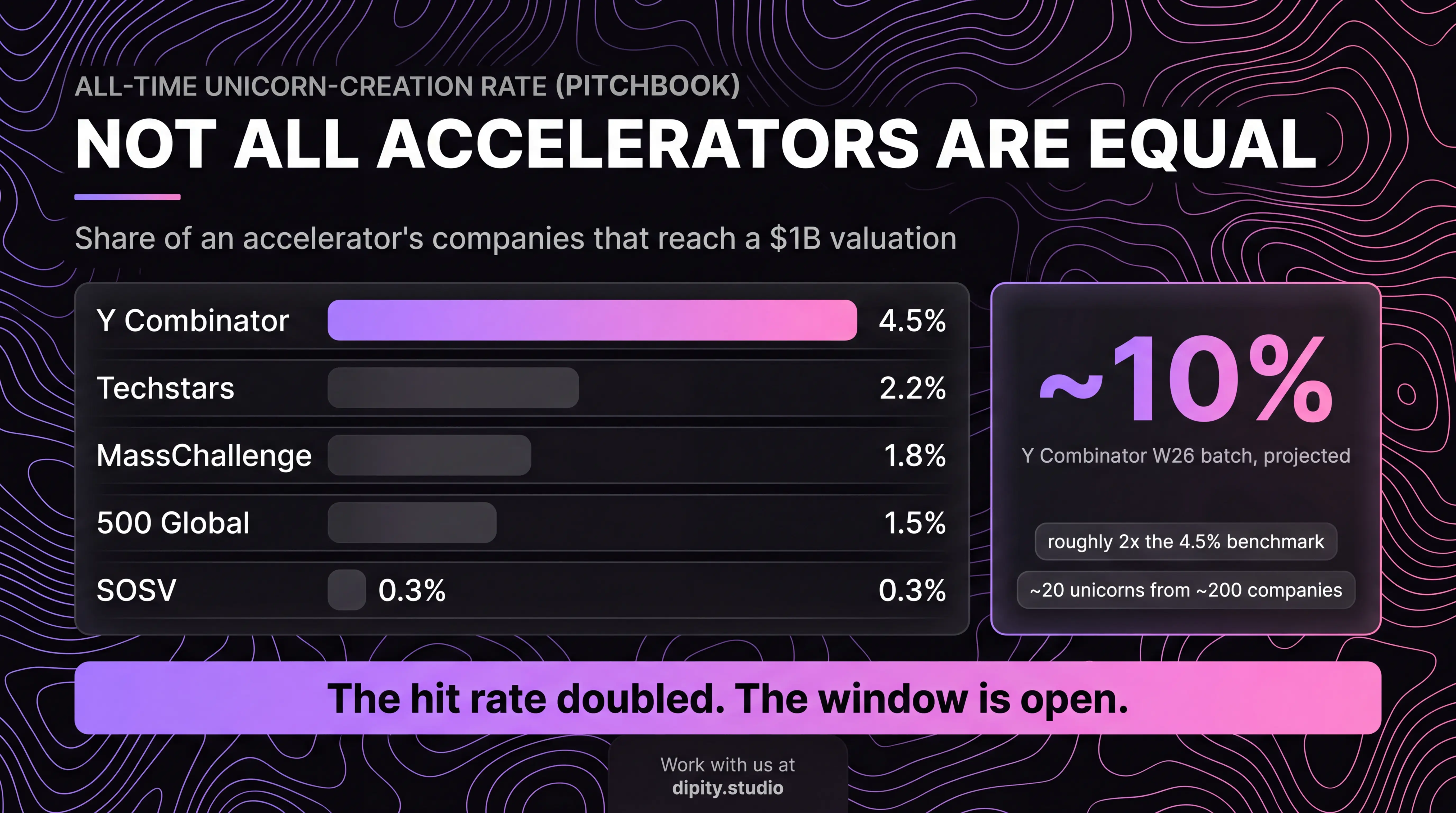

Y Combinator's unicorn rate has climbed steadily for 15 years: roughly 4% for 2010 to 2014 batches, about 5% for 2015 to 2018, and a projected 10% for W26. The long-run number most analysts cite is 4.5% of all YC companies ever funded reaching a billion-dollar valuation, which PitchBook confirms is the highest unicorn-creation rate of any accelerator, ahead of Techstars at 2.2%, MassChallenge at 1.8%, 500 Global at 1.5%, and SOSV at 0.3%.

The year-over-year picture, drawn from Rebel Fund's analysis of every YC batch:

• 2010 to 2014 batches: ~4% unicorn rate, already 4x the venture-backed baseline.

• 2015 to 2018 batches: ~5%, a 25% improvement on the prior era.

• 2016 specifically: ~9%, with the W16 batch reaching an 11% unicorn ratio.

• All-time: 101 YC unicorns had already been minted by August 2022, and the count has kept climbing since.

• W26 projection: ~20 unicorns from ~200 companies, roughly 10%, with the batch 64% B2B and tilted toward robotics, energy, and infrastructure.

Two details make the W26 projection more credible than hype. First, YC's rate has beaten each prior era consistently, so 10% is a continuation of a 15-year slope rather than a break from it. Second, YC is simultaneously narrowing its funnel, bringing Startup School back on July 25 and 26 as an invite-only event where hand-selected builders are flown to San Francisco. As Lenny Rachitsky's breakdown of YC's inner workings documents, the accelerator's edge has always been selection plus system, and both levers are tightening at once.

How Does the Founder Institute Compare to Y Combinator on Unicorn Production?

The Founder Institute operates earlier and wider than YC, and its current cohort math has converged on the same 10% expectation. The Founder Institute is the world's largest pre-seed accelerator, running programs across 200 cities on six continents, with 7,500+ graduated companies that have collectively raised over $2B. Where YC takes companies, FI takes people, often before incorporation, which makes its hit rate math harder to compare directly but its wins more striking.

Two portfolio cases show the ceiling. Udemy came through the Founder Institute portfolio and went public on the NASDAQ in October 2021, raising $421M in its IPO. Esusu, the rent-reporting fintech, became a unicorn in January 2022 on the back of a SoftBank Vision Fund 2-led $130M Series B. Both started as pre-seed founders inside a structured program, not as anointed serial operators.

The current cohort is where the numbers get interesting. This session drew 1,500 applications and accepted 50 founders, several of them co-founder pairs sharing a single company, which puts the acceptance rate near 3% and the true company count below 50. The internal expectation communicated to the cohort is 3 to 5 billion-dollar companies from the group. Run the division and you land on roughly a 10% unicorn expectation, the same number VCs are projecting for YC W26 from a completely different selection process. When two independent systems converge on the same output rate, the reasonable conclusion is that the production function changed, not that everyone got lucky at once.

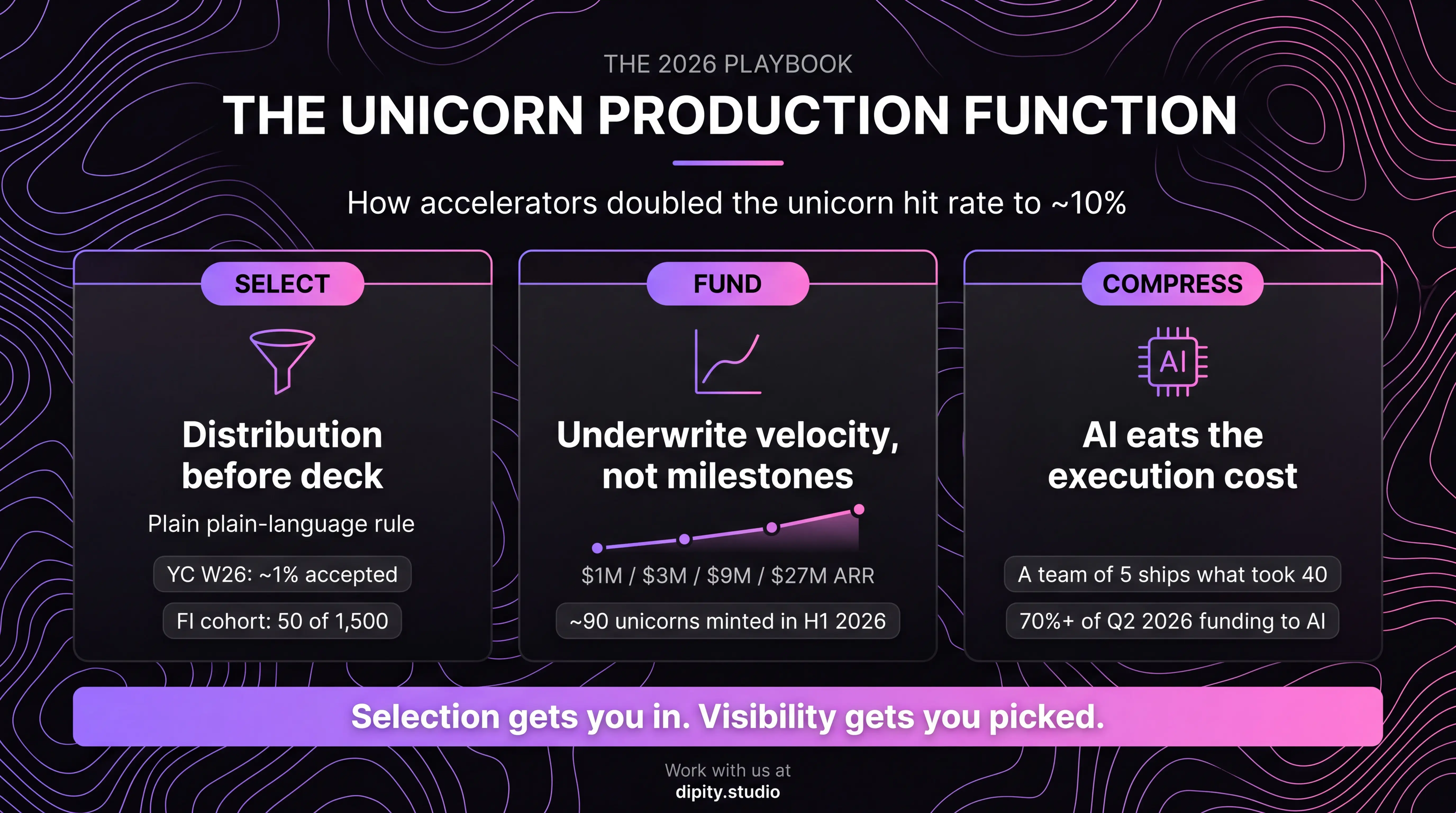

What Playbook Are VCs Actually Using to Compress the Unicorn Timeline?

The 2026 playbook has three moving parts: pick founders with existing distribution, fund them to velocity benchmarks instead of milestones, and let AI eat the execution cost. The clearest evidence of how far this has gone landed this week, when Lyzr, an enterprise AI agent startup, let its own AI agent run point on its $100M Series B, fielding questions from more than 130 investors and drafting the investment memos. The fundraise itself became the product demo.

The funding side of the playbook changed just as much as the execution side. TechCrunch's analysis of the current cohort of breakout companies found top AI startups compounding revenue faster than any prior software generation, with one adding its second $100M in ARR in just two quarters. Investors responded by underwriting velocity itself rather than traditional milestones, which resets the benchmark every seed and Series A founder gets measured against. A founder entering an accelerator in 2026 is not being compared to the 2019 version of their company. They're being compared to the fastest revenue curves in software history, and the capital flows to whoever looks capable of matching them.

For founders, the practical reading of the playbook comes down to a few behaviors that the funded 10% share:

• They're visible before they raise. Investors track founders for months before a round opens. Buyers behave the same way, and buyers today are buying based off of the CEO or founder they have on their social feed. Then they get curious about the product. Not the other way around.

• They publish their math. Velocity-underwritten capital needs legible numbers, and founders who show revenue mechanics in public get benchmarked up, not down.

• They treat the program as distribution, not education. A cohort is a concentrated network of future customers, hires, and co-investors, and the founders who convert it treat every session like a channel.

Research backs the visibility point specifically. The Edelman-LinkedIn B2B Thought Leadership Impact Report has repeatedly found that a majority of decision-makers judge a company by the quality of its leadership's public thinking, and Weber Shandwick's research attributes 44% of a company's market value to CEO reputation. The playbook works because the market prices the founder before it prices the product.

Why Does Founder Authority Decide Which Cohort Companies Become the Unicorns?

Because selection is no longer the differentiator inside a cohort. Everyone admitted has already survived a 97 to 99% filter, so the separating variable becomes who the market can see. Inside a group where every company has a credible team and a fundable idea, the 3 to 5 that break out are disproportionately the ones whose founders compound attention into pipeline, talent, and investor pull between demo days.

This is the entire thesis Dipity is built on, and it's why the unicorn-rate data matters to founders who will never apply to an accelerator. If visibility is what separates outcomes inside the most filtered rooms in tech, it separates outcomes even harder outside them.

"We didn't join the Founder Institute to collect a certificate. The projection says 3 to 5 companies in this cohort become unicorns, and my job for the next 18 months is to give Dipity a real shot at that list. Putting our targets in public is how we keep ourselves honest about the work."

— Morgan Von Druitt, Founder, Dipity

The mechanism is not mysterious. A founder who publishes real thinking weekly shows up in the feeds, searches, and AI-generated answers of every buyer, hire, and investor evaluating the space, and each of those audiences de-risks the company a little more. Run that loop for 18 months and the company raises faster, hires better, and closes earlier than an identical company led by a silent founder. The cost of skipping it compounds just as quietly in the other direction.

The cascade matters as much as the volume. Prospects who see a founder's thinking convert warmer and earlier in the cycle. Peers cite the work, which multiplies reach without spend. Candidates apply because they can evaluate who they'd be working for before the first call, which is a hiring advantage no compensation package replicates at the early stage. And investors, who track founders for months before a round ever opens, arrive at the first meeting already partly convinced. Every stage of that cascade was already true in the last cycle, but the 10% era raised the price of ignoring it, because the cohort peers who do run the loop are now setting the pace the silent founders get measured against.

What Is Dipity Targeting, and What's the Math?

Dipity is aiming to be one of the 3 to 5 billion-dollar companies this Founder Institute cohort is projected to produce. That's a goal we're working toward, not a guarantee, and here is the 18-month plan we're running to give ourselves a real shot. A goal without numbers is a slogan, so these are the milestones, published where anyone can check them later.

Our product is Sera, a founder-authority platform that installs a founder's actual voice, ICP, pillars, and competitive position, then runs the content engine on top of it. Today we serve it as a 14-day sprint that hand-trains each founder's Sera, and we're raising a $500K to $2M seed to turn that hand-trained engine into self-serve software. Every manual sprint is the data wedge for the platform. Here is what the 18 months are aimed at:

• Now: bootstrapped at roughly $4K MRR, five months in, with a 12+ founder beta cohort (operators who held exec roles at Citi, Forbes, AMD, and IBM, plus a YC founder) hand-training their Sera.

• Seed ($500K to $2M): ship self-serve Sera v1, turning the hand-trained engine into software any funded founder can run.

• 18-month target: convert the beta cohort and the accelerator pipeline into paying SaaS accounts, stand up the proprietary founder-intent data layer, and work toward $1M ARR, the entry point of the T2D3 venture curve.

• Beyond: prove the founder-to-founder network (capture, connect, capitalize) and run the T2D3 sequence, triple, triple, double, double, toward the revenue that underwrites a billion-dollar outcome.

The unicorn math works backward from the venture benchmark. A $1B valuation at today's software multiples implies roughly $65M+ ARR at scale, and the standard path there is the T2D3 curve: reach ~$1M ARR, then triple, triple, double, double. The 18-month job is reaching the entry point of that curve. The opening is real: there are more than 25,000 funded B2B SaaS startups, each needing a founder voice, and almost none can justify a $15K to $20K per month agency retainer. Sera is priced for a first-time funded founder, which is the whole point.

We pitch in California August 17 to 27, and the numbers above will be checked against reality in public either way. The honest trade-off deserves stating too: a 10% expectation still means 90% of a hand-picked cohort falls short of the label, and a company can miss the unicorn mark while still becoming an excellent business. The commitment is to the work and the transparency, not to a vanity valuation at any cost.

Conclusion: The Hit Rate Doubled. The Window Is Open.

The data says something has structurally changed in how billion-dollar companies get made. Y Combinator's unicorn rate climbed from 4% to 5% to a projected 10% across 15 years of batches, the Founder Institute's current cohort carries the same 10% expectation from a different direction, and record capital plus AI execution collapsed the timeline from a decade to a few years. The founders who capture this window share one visible trait: the market knows who they are before it knows what they sell.

Dipity exists to build that visibility for funded B2B SaaS founders, and we're now running the same playbook on ourselves inside the Founder Institute, in public, with the targets written down. If you're a founder staring at this window and wondering whether your own visibility is the bottleneck, that's exactly what we built Sera to fix. Work with us at dipity.studio.

Frequently Asked Questions

What percentage of Y Combinator companies become unicorns?

Roughly 4.5% of all YC companies across its history have reached billion-dollar valuations, the highest rate of any accelerator per PitchBook. Batch-era analysis from Rebel Fund shows ~4% for 2010-2014 batches, ~5% for 2015-2018, and VCs are projecting roughly 10% for the W26 batch.

How many unicorns has Y Combinator produced in total?

Rebel Fund counted 101 YC unicorns as of August 2022, and the number has continued climbing since, with YC reporting more than 100 unicorns across 5,000+ funded companies.

What is the Founder Institute and how does it differ from YC?

The Founder Institute is the world's largest pre-seed accelerator, operating in 200 cities across six continents with 7,500+ graduated companies that have raised over $2B. It admits founders earlier than YC, often pre-incorporation, and its notable outcomes include Udemy's NASDAQ IPO and Esusu's 2022 unicorn round.

How long does it take to become a unicorn in 2026?

The historical average was 7 to 10 years, but nearly 90 unicorns were minted in H1 2026 alone, many by AI companies reaching the mark in 2 to 4 years, driven by record capital and AI-compressed execution.

What revenue does a startup need for a $1B valuation?

At prevailing software multiples, roughly $65M+ ARR, though high-growth AI companies have commanded far higher multiples. The standard path is the T2D3 curve: reach ~$1M ARR, then triple, triple, double, double.

Is a 10% unicorn hit rate realistic for accelerator cohorts?

It's a projection, not a guarantee, but it's supported by two independent data points: VC projections of ~20 unicorns from YC's ~200-company W26 batch, and the Founder Institute's 3-to-5-unicorn expectation from a ~50-founder cohort. Both double the 4.5% historical benchmark.

Works Cited

Crunchbase News. (2026, July). Global startup investment hit record $510B in H1 2026 as AI boom accelerates funding and exits. Link

Edelman & LinkedIn. (2024). B2B thought leadership impact report. Link

Founder Institute. (2026). Global portfolio of graduates. Link

Heyman, J. (2022, August). On 101 Y Combinator unicorns. Rebel Fund / Medium. Link

PitchBook. (2021). Y Combinator leads among accelerators in unicorn-creation rate. Link

Rachitsky, L. Pulling back the curtain on the magic of Y Combinator. Lenny's Newsletter. Link

TechCrunch. (2026, July 5). Almost 90 new unicorns have been minted so far this year. Link

TechCrunch. (2026, July 8). These AI startups are growing revenue at faster and faster rates. Link

TechCrunch. (2026, July 9). An AI agent startup just let its agent run its $100M fundraise. Link

The VC Corner. (2026, June). YC W26 Demo Day: complete breakdown. Link

Weber Shandwick. The CEO reputation premium: Gaining advantage in the engagement era. Link

Y Combinator. (2026). Startup School 2026. Link

.svg)

Get weekly updates

*We’ll never share your details.

Follow us — @Dipity

Join Our Newsletter

Get a weekly selection of curated articles from our editorial team.