What Do Investors Actually Check Before a 2026 Raise? Why Founder Authority Now Shows Up in Diligence

Founder due diligence now includes your digital footprint. What VCs actually check before a 2026 raise, with data from HBR, DocSend, PitchBook, and Crunchbase.

What Do Investors Actually Check Before a 2026 Raise? Why Founder Authority Now Shows Up in Diligence

What Do Investors Actually Check Before a 2026 Raise? Why Founder Authority Now Shows Up in Diligence

By Morgan Von Druitt · July 2026 · 8 min read

TL;DR Founder due diligence in 2026 starts with the founding team and ends with your digital footprint, not the other way around your deck assumes. Harvard Business Review's landmark VC survey of nearly 900 venture capitalists found investors rank the founding team as the single most important factor in deal selection, ahead of product, market, and business model. At Dipity, we prepare seed-to-Series-B founders for exactly this screen, because the diligence trail investors walk now includes everything you've published, said, and been cited for online.

Last month a founder told me his raise died in a partner meeting he never attended. The associate loved the metrics. The partner searched the founder's name, found a dead LinkedIn page, two posts from 2024, and zero third-party mentions, and moved on to the next deal in the queue. No feedback email mentions this. It shows up as "not a fit right now." That invisible screen is what this piece is about.

What Do VCs Look at First When Your Deal Hits Their Inbox?

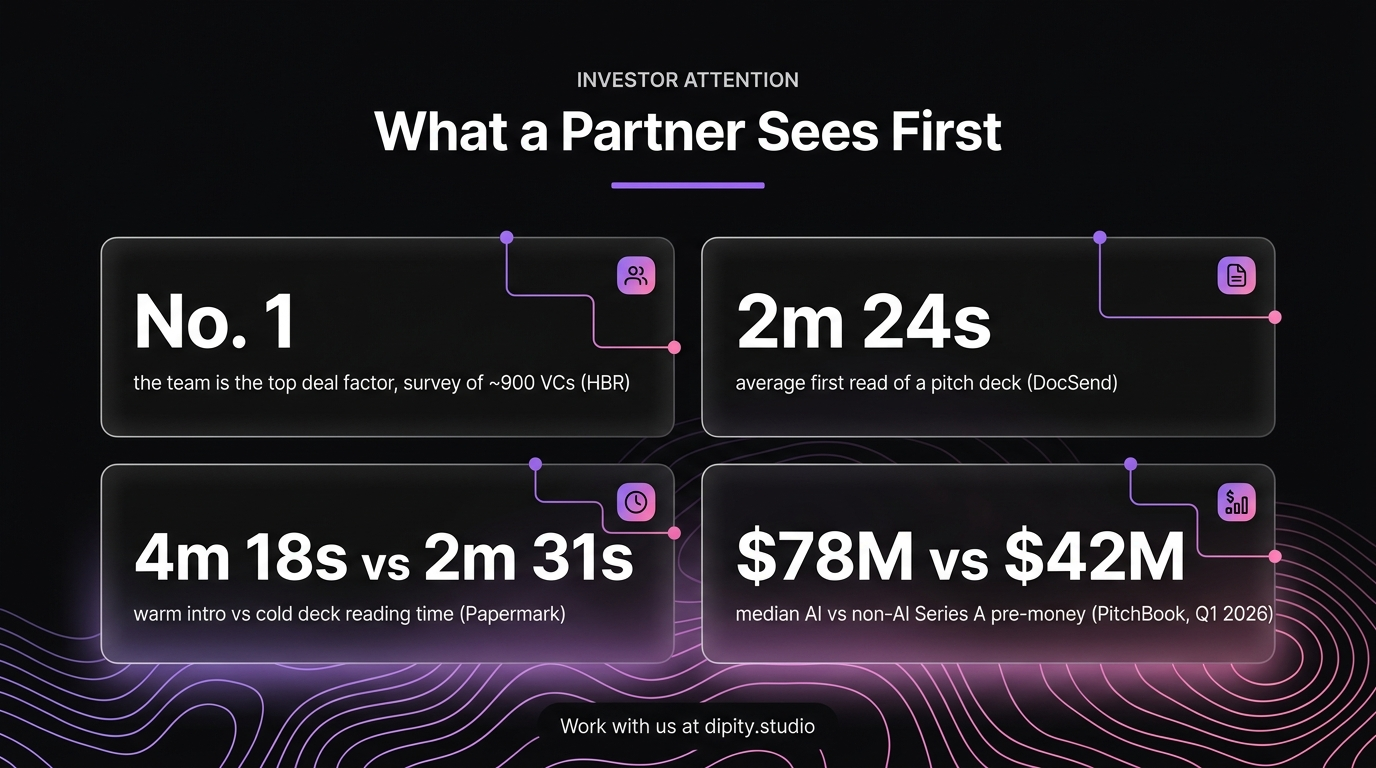

The team, and they decide fast. VCs rate the founding team as the most important selection factor, and the median investor spends under two and a half minutes on a first read of your deck. The person, not the product, absorbs most of that attention window.

The evidence base here is unusually strong. The Gompers, Gornall, Kaplan, and Strebulaev survey published in Harvard Business Review asked nearly 900 VCs what drives their decisions; the founding team ranked first both when picking deals and when explaining, in hindsight, why deals succeeded or failed. The full working paper shows the same result across stage, sector, and fund size.

Attention data tells you how little time you get to prove it. DocSend's pitch deck research has tracked investor reading time for years; recent editions put the average first read near 2 minutes 24 seconds, and Papermark's 2024-2025 dataset found decks shared through a warm introduction get read for 4 minutes 18 seconds versus 2 minutes 31 seconds cold. Nearly double the attention, purchased entirely by who vouches for you and what the investor already knows about your name.

Which means the real first screen happens before the deck opens. It happens when a board member shares one of the founder's posts. It happens when an investor reads a white paper and uses that as the segue into a cold DM.

Where Does Founder Authority Show Up in the Diligence Process?

In the background check nobody tells you about. Beyond references and records, investors review your public digital presence for consistency, credibility, and red flags. A published body of work reads as evidence; an empty profile reads as risk.

Diligence firms have productized this. KPMG's due diligence research describes the digital footprint as a core diligence surface: what a founder has published, how they respond under pressure, and whether the public record matches the deck's claims. Academic work backs the effect; a Review of Financial Studies study of roughly 2,000 applicants to a UK seed fund found diligence processes dig well past financials and materially change growth outcomes for the companies screened.

What investors report finding falls into three buckets:

- Corroboration. Do podcasts, posts, and press repeat the same numbers and story the deck tells? Inconsistency kills deals quietly.

- Category signal. Is the founder cited by others, invited onto podcasts, quoted in trade press? Third-party validation compounds.

- Temperament. How does the founder handle public disagreement? Partners read comment sections more than founders think.

Your profile authority is the biggest signal or precursor of your success when you're looking to raise or hire top talent. Investors formalized that instinct into process; most founders still haven't formalized the response.

What Is the Valuation Math on Founder Reputation?

Reputation carries a measurable share of enterprise value. Executives attribute 44% of a company's market value to CEO reputation, and in 2026's AI-skewed market, credibility premiums show up directly in round pricing.

Start with the foundational number. Weber Shandwick's CEO Reputation Premium study found global executives attribute 44% of their company's market value to the reputation of the CEO. Treat it as directional rather than precise and the implication holds: on a $40M pre-money, roughly $17.6M of perceived value rides on the person across the table.

Now layer on what 2026 pricing already shows. PitchBook-NVCA Venture Monitor data put the median Series A pre-money valuation for AI companies at $78.0M against $42.4M for non-AI companies in Q1 2026. That $35.6M gap is a narrative premium as much as a technology premium, and narrative is priced through the person who tells it. The founders capturing the top of that range arrive with a public record that makes the story verifiable before diligence starts.

I've seen the inverse cost founders real money. A strong product with an invisible founder gets priced on metrics alone, and metrics at seed are always thin. The metric that matters ultimately is valuation, and valuation is a trust calculation.

How Does 2026's Capital Concentration Change the Screen?

Concentration made the screen harsher. With a record $510B raised in H1 2026 and 43% of it absorbed by two companies, the remaining capital gets allocated with more scrutiny per check, and strategic investors doing the allocating diligence reputation hardest of all.

The numbers are stark enough to reprice everyone's assumptions. Crunchbase's H1 2026 report recorded $510B in global venture funding for the half, with OpenAI and Anthropic alone absorbing roughly $217B, about 43% of all startup capital raised worldwide. Everyone else competes for the remainder against a higher bar of proof.

Look at who wrote the biggest checks outside the labs during the first week of July: National Grid Ventures put $1.75B into Joulent, and Salesforce led 8090's $135M Series A. Strategic and corporate investors move on longer diligence cycles, involve more stakeholders, and weight founder reputation heavily because their brand attaches to yours at announcement. Getting on a strategic's radar in the first place is a visibility problem; surviving their diligence is a consistency problem.

For a seed or Series A founder, the takeaway is direct. The capital exists, the bar moved, and the founders clearing it are the ones whose public record does part of the diligence for the investor.

How Do You Build the Diligence Trail 90 Days Before the Raise?

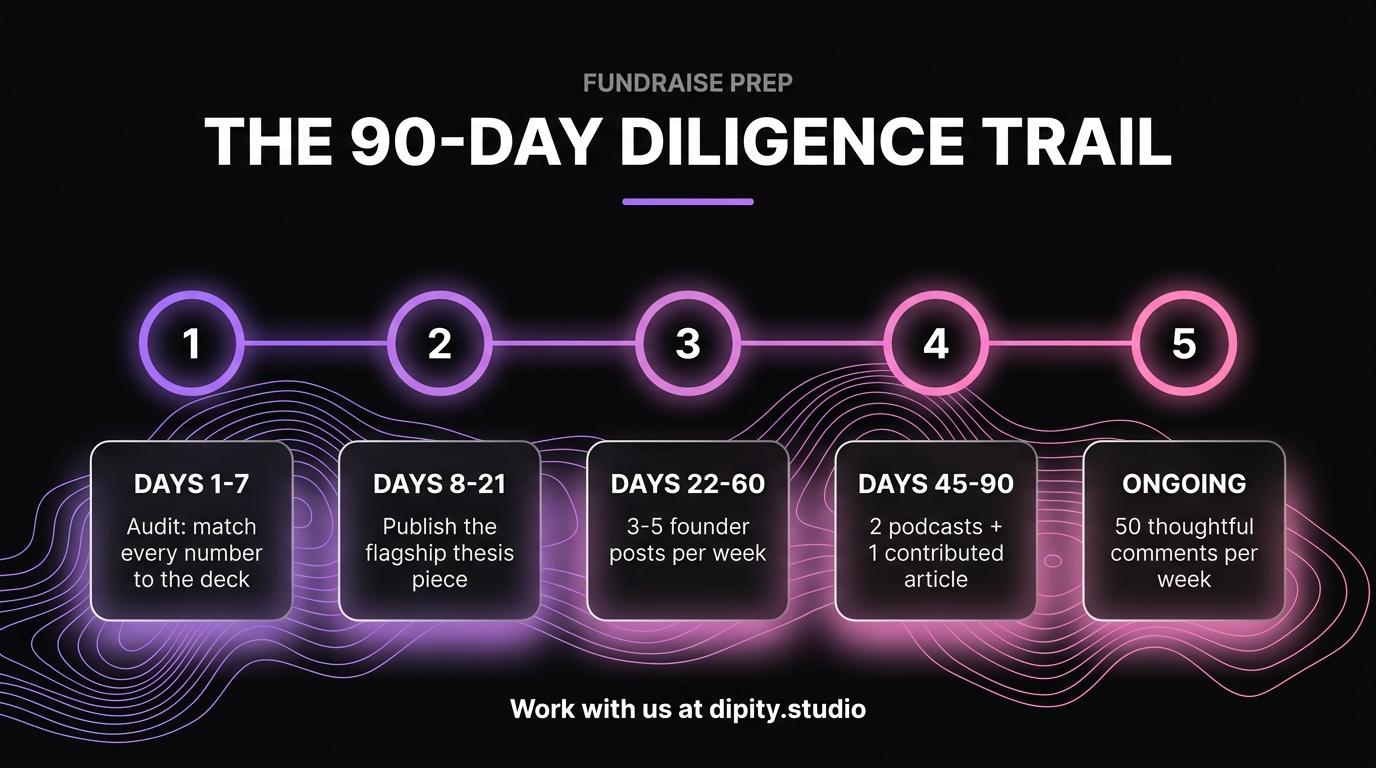

Work backwards from what the partner will find. Ninety days is enough to turn a dead digital footprint into a corroborating one: a flagship point-of-view piece, a consistent posting cadence, two podcast appearances, and a profile that matches the deck's story line for line.

Here's the sequence I run with founders heading into a raise window:

- Days 1-7: audit and align. Search your own name the way a partner would. Fix the LinkedIn headline, the about section, and every number so they match the deck exactly.

- Days 8-21: publish the flagship. One pillar piece stating your category thesis, with sourced data. This is the artifact diligence finds and the anchor every later post links back to.

- Days 22-60: run the cadence. Three to five posts a week in the founder's real voice, each carrying one insight an investor would flag as pattern recognition. Consistency reads as operational discipline.

- Days 45-90: borrow third-party surfaces. Two podcast appearances and one contributed article put independent corroboration into the record. Investors discount what you say about yourself and index what others publish about you.

- Ongoing: engage like an operator. Fifty thoughtful comments a week on the feeds your investors and buyers read builds recognition before the intro email lands.

Notice what's absent: follower counts. Impression farming is a surefire way to build a large audience that never wants to buy from you, and investors read hollow reach the same way buyers do. Depth of position beats breadth of audience on every diligence screen I've watched founders pass. My breakdown of why your face is the best go-to-market channel covers the full engine this sequence plugs into.

What Should You Do Before Your Next Raise?

Treat founder authority as a fundraising workstream with a 90-day lead time, the same way you treat your data room. The investors you want already treat it as one.

Founder silence is the most expensive line item on the cap table. The full picture from the research is hard to argue with: team ranks first in VC decision-making per Harvard Business Review, attention per deck is measured in seconds per DocSend, digital footprints are formal diligence surfaces per KPMG, and reputation carries 44% of perceived market value per Weber Shandwick. Every one of those screens is buildable in advance, and almost none of your competitors are building for them.

That's the gap the Sera Implementation Sprint closes: two weeks to install your voice, your category position, and the publishing engine, so the diligence trail exists before the raise begins. Talk to me at dipity.studio and I'll walk you through what investors will find today, and what they should find in 90 days.

Frequently Asked Questions

Do investors really check a founder's social media before investing?

Yes, as a standard part of background diligence. KPMG and other diligence practices treat the digital footprint as a formal review surface, covering published content, press mentions, and public conduct. An empty or inconsistent record doesn't disqualify you outright; it removes corroboration your competitors will have.

How much of a raise decision is the team versus the product?

The HBR survey of nearly 900 VCs found the founding team is the most important factor in both selecting deals and explaining outcomes afterward. Product, market, and business model matter, and the team still outranks them at early stage where evidence is thin.

What red flags do investors find in founder digital footprints?

The common ones: numbers online contradicting the deck, long silent gaps suggesting a stalled company, combative behavior in public threads, and zero third-party mentions. Consistency issues damage more deals than controversial opinions do.

Is 90 days really enough to build founder authority before a raise?

Ninety days builds a credible, corroborating trail: a flagship thesis piece, a steady cadence, and independent third-party appearances. Deep authority compounds over years, and a partner searching your name in month four finds a living operator instead of a ghost, which is the bar the raise actually requires.

Does founder authority matter more for AI startups than other sectors?

The premium is larger. PitchBook-NVCA data shows median AI Series A pre-money valuations near double non-AI equivalents, and that spread is priced through narrative credibility. In a category where every deck claims AI capability, the verifiable founder position is the differentiation.

Sources

- Crunchbase News — Global startup funding H1 2026 report

- DocSend — Pitch deck metrics: startup index

- Harvard Business Review — How Venture Capitalists Make Decisions (Gompers, Gornall, Kaplan, Strebulaev)

- NBER Working Paper 22587 — How Do Venture Capitalists Make Decisions?

- KPMG — Due diligence and the digital footprint

- Papermark — Pitch deck metrics report 2024-2025

- PitchBook-NVCA — Venture Monitor, Q1 2026

- PR Newswire — National Grid Ventures invests $1.75B in Joulent

- Review of Financial Studies — Broader role of venture capital due diligence

- Weber Shandwick — The CEO Reputation Premium

.svg)

.jpg)

Get weekly updates

*We’ll never share your details.

Follow us — @Dipity

Join Our Newsletter

Get a weekly selection of curated articles from our editorial team.